Brands are often founded with the purpose of aligning with a given trend and exploiting a perceived white space in the market. In the mid-2000s, introducing a premium bourbon may have seen high growth, likewise for rolling out a specialty high-end tequila in the early to mid-2010s. But when founders really get it right, and their offering is able to align with multiple trends at once, it’s possible to see uniquely explosive growth. Such was the case for Surfside, which saw over a million cases sold over the course of a year between 2022 and 2023.

Surfside is a Philadelphia-based ready-to-drink brand rolled out by the creators of Stateside Vodka. With RTDs taking center stage as the spirits industry’s spotlight category, Surfside was able to build on this platform to leverage consumer interest in flavor variety, health consciousness, and convenience into the highest-growth brand in the United States.

On this episode of the Park Street Insider Podcast, Emily Pennington is joined by Clement Pappas, CEO of Stateside Brands. The two discuss how Surfside went from concept to can to achieving astronomical sales in just a few years. They’ll explore the brand’s unique route-to-market strategy and how they dealt with demand and scaled the business.

The Latest Cocktail Trends with Matt Ray From Sazerac

Matt Ray, Experience Lead at Sazerac House, discusses the latest cocktail trends and their effect on the on-premise. Ray touches on the top cocktails, trending non-alcohol alternatives, and why consumers are trading up.

Top Five Major Alcohol Trends in the News

Ferron Salniker, Spirits Editor at BevNet, discusses the top five major alcohol trends in the news this year. Ferron touches on the rise of NA, the RTD boom and Sazerac’s acquisition of BuzzBallz, and more.

Current Alcohol Business Models

Emily Pennington, Senior Manager, Content & Education at Park Street Companies, discusses current alcohol business models. Pennington discussed how brands have shifted away from a reliance on traditional distribution models and on-premise bars, using BuzzBallz as a case study.

2024 has been a challenging year in the alcohol category. While beer and wine have both seen declines, spirits have managed to achieve positive growth in value (+0.3) and volume (1.7%) for the 52 weeks ending August 10, per a recent Nielsen IQ webinar. However, said growth was driven solely by RTDs, as removing these from the category’s off-premise performance reveals a 0.4% volume loss for the same period.

Where Are Alcohol Consumers Shopping?

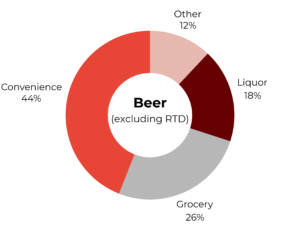

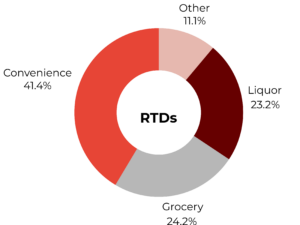

Consumers are choosing to shop at familiar channels that offer them value for money and convenience. The convenience store channel is driving quite a bit of growth, increasing its dollar sales by 1% compared to a year ago. Mass merchandise stores and dollar clubs are also performing well as a group, increasing dollar sales by 0.4%, while liquor stores and grocery stores have both seen a decline in sales so far this year.

The strong performance of the convenience channel is driven by RTDs and beer, as these locations offer a friction-free environment to quickly and easily purchase these categories. With consumers showing an inclination to shop both close to home and in close proximity to the time of consumption, the familiarity and ease of convenience stores have made them a go-to. 41% of all RTD purchases off-premise occur in convenience stores- more than any other channel.

Convenience is such a driving force that C-stores are actually growing via all of the spirits, wine, and RTD categories. Recent developments in spirits-based RTD legislation have made the category increasingly available in C-stores, contributing to a loss in volume for open-state liquor stores.

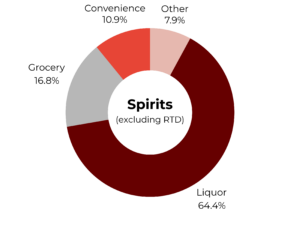

But make no mistake—for spirits, the liquor store is still the preferred shopping destination. On the whole, liquor stores claim a 65% share of off-premise purchases for the spirits category (excluding RTDs), where consumers appreciate the variety and selection-driven nature of these locations. Grocery stores and convenience stores are the next two most shopped locations for spirits, claiming 17% and 11% shares, respectively.

To combat some of the losses in U.S. liquor stores, there has been an increase in promotions and discounts, bringing the average price per unit down 1.4% between January 2023 and August 2024. The goal is to drive foot traffic and get people in the door. Yet, certain categories in the liquor store channel remain significant opportunities to target. Non-alcoholic spirits, wine cocktails, spirits-based RTDs, and Tequila are all strong growth drivers in the liquor channel, while hard seltzers, wine, rum, and cognac are seeing the most significant category declines within the liquor store channel.

Dollar Share by Channel

Source: Nielsen IQ

Alcohol Trends in Key States in 2024

In California, the largest beverage alcohol market in the United States, spirits-based ready-to-drink cocktails have seen 37% growth compared to one year ago. This market tends to stay ahead of the curve for emerging flavors as well. It’s also one of the strongest markets for the tequila category, with 27% of all spirits dollars spent in the state dedicated to the tequila category.

Texas is among the more interesting off-premise markets, as categories that have struggled nationwide have found pockets of growth within the state. This is particularly true with cognac, which has grown by 2% in the state as opposed to one year ago. The same can be said for below-premium beer, which is up 6%. The agave spirits and spirits-based cocktail segments each showed 8% growth compared to one year ago.

Off-premise stores in New York have an extensive depth of selection within the wine category and whiskey subcategory. There are more than 30k wine UPCS in the state. Although whiskey is the number one spirits category in New York, it has lost ground to Tequila and Mezcal which have grown a combined 4% across off-premise liquor stores. The state is home to an outsized number of high-volume spirits stores that have an emphasis on a diverse selection of spirits items.

Meanwhile, in New Jersey, some spirits categories that are seeing national declines are trending positively. Brandy and rum, for example, have grown by 5% and 4%, respectively. New Jersey’s liquor store channel has been particularly profitable for RTD spirits cocktails which have grown by 24%.

In Florida, the categories that are out of favor according to national data but have found pockets of growth include whiskey, which has seen a 3% increase year-over-year in the state. Likewise, still wine is doing quite well in Florida’s liquor store channel, offering 2% growth through August 10. Due to the notable influence of Hispanic culture in the state, the state has become one of the largest opportunities for agave spirits brands. Tequila and mezcal have seen an impressive growth rate of 15% year over year while imported beers have also increased by 4%.

Despite a slowdown in overall investment, the first half of 2024 saw several significant mergers and acquisitions in the beverage alcohol sector. Strategic buyers, and even several private buyers, capitalized on evolving consumer trends and market opportunities. A total of 34 noteworthy deals were recorded during this period.

Spirits led the pack with 22 deals, reflecting the category’s ongoing popularity and innovation. Wine followed with 7 deals, while the beer saw 5 transactions. This distribution highlights the spirits category’s continued dominance in M&A activity, particularly in areas such as premium tequila, craft whiskey, and ready-to-drink (RTD) offerings.

The first half of the year saw 7 deals in the booming RTD and canned cocktail segments, emphasizing premium offerings. As consumer preferences continue to evolve and the industry adapts to post-pandemic market conditions, future M&A activity in the beverage alcohol space will likely focus on innovative products, direct-to-consumer capabilities, and brands that resonate with younger consumers.

Drinks Industry M&A in H1 2024

Spirits Category Deals

Diageo Became the Sole Owner of DeLeón Tequila

The Artisanal Spirits Company Acquired Single Cask Nation

InvestBev Backed JuneShine with seven-figure Investment

Next Century Spirits Took Stake in Vide RTD

Heritage Distilling Co. Acquired Thinking Tree Spirits

CoreBev Expanded Portfolio with Strategic Acquisition of Continuum Distilling

Distill Ventures Invested in Two Female-Owned Brands, Jackson McCrea Whiskey and Ume Plum Liqueur

Illva Saronno Completed Full Acquisition of Engine Gin

While extensive experience in the alcohol industry can be advantageous for launching a new brand, some of the most disruptive and game-changing brands have emerged from founders with little to no prior industry experience.

So how have these entrepreneurial newcomers managed to achieve success despite being industry outsiders? The Park Street Insider Podcast has hosted many successful founders, offering insights into how they educated themselves and navigated the complex world of alcohol branding and regulations.

Do Your Research and Hire a Good Attorney

In 2019, the founders of 21 Seeds tequila identified an untapped market opportunity for a premium, female-centric flavored tequila. Capitalizing on flavor innovation, a health-conscious ethos, and aspirational messaging, the brand quickly resonated with its target consumers. Just three years after launch, 21 Seeds was acquired by Diageo in 2022.

The US alcohol industry is highly regulated and complex, so a good alcohol attorney will educate you on the basics you need to know starting out. “We had so many questions and we wrote them all down ahead of time because we did not want to waste one single minute and pay for one extra minute of her time,” said Hantas.

After hiring an attorney, Hantas says the 21 Seeds team spoke to anyone and everyone they knew with some familiarity with the alcohol industry, including retailer, restauranteurs, packaging etc., to ask questions. “We read everything we could read. I mean it was like we did a masterclass in spirits. Like we learned everything we could learn in a very short amount of time. But we were so excited by what we were doing that we were up all night doing it.”

What were they using? “You can learn everything that you need to learn on YouTube and Google, including the very first GSM I ever did. I had no idea how to do that. I was like, what do you even present? And I Googled general sales meeting in spirits and sure enough, up pops a GSM. And so that was how I figured out how to outline my GSMs.”

Buzzballz an early leader in the current ready-to-drink category, provides another example of an outsider-turned-insider success story. Launched in 2009, Buzzballz has since grown into a leader in the RTD category, selling over 1 million cases in 2023. As a result, Sazerac acquired the brand in 2024.

When Buzzballz founder Merrilee Kick, a high-school teacher from Texas, decided to create her brand, she had to build her knowledge base from the ground up. “I got into it by just Googling and researching how to build an alcoholic beverage. I didn’t know what I was doing,” said Kick. “Honestly, I was just fiddling around trying to find a way to make some money.”

Kick’s fact-finding mission eventually led her to the TTB’s Beverage Alcohol Manuel (BAM), where she was able to answer key questions and formulate a plan. The BAM “basically goes through the rules and regulations on eting and advertising alcoholic beverages. So, what are the standards of fill? How much headspace can you have? What kinds of things are required to be on the label? What kinds of things can you put on a formula? How do you get a formula?

Hard work and attention to detail paid off for Kick who was able to navigate the TTB’s initial processes. “I was probably one of the fastest people to get a basic permit with a TTB. I ended up from start to finish taking only six months to get a basic permit, but you have to get your basic permit before you can get your winery permit or your distillery permit or your malt permit. So you have to start with a basic permit and I got my distillery and my winery and my basic permit in six months.”

Listen to the full episode here:

Find Paths to Connect With Industry Members

Ten To One Rum has grown significantly and helped bring new consumers into the rum category. The brand partnered with award-winning singer Ciara who became a co-owner of the brand in 2021. In 2022 the Diageo-backed brand incubator, Pronghorn, bought into the Caribbean-based brand, followed by a $1 million investment through private equity first InvestBev.

Marc Farrell, founder of Ten To One Rum and former Starbucks executive, initially drew upon his experiences as an engaged consumer to formulate his premium Caribbean rum brand’s distinctive flavor profile.

“I spent countless hours at rum bars, sampling products and soliciting feedback from knowledgeable bartenders,” he recalls. “I remember going to Rumba which is in Seattle, very famous rum bar, and spent a lot of time in there trying different products, different SKUs, talking to the bartenders about what they liked and didn’t. Then going through it on our side with some trial and error and the creation of our blends.”

Farrell was keen to distinguish between necessary learning that’s done for product development and the knowledge needed to run the business side of things. He also sought out industry members with deep industry credentials to help inform his decisions.